A roof leak after wind and rain hits different. It is not just water on the floor. It is that sinking feeling of “How bad is this?” mixed with “What do I say to insurance so I do not screw this up?”

If you are in the Atlanta metro and you have active leaking, ceiling stains, wet drywall, or attic moisture after a storm, the next 24 hours matter. Not because you need to panic. Because this is the window where good documentation protects your insurance claim and bad documentation turns into delays, denials, or lowball estimates.

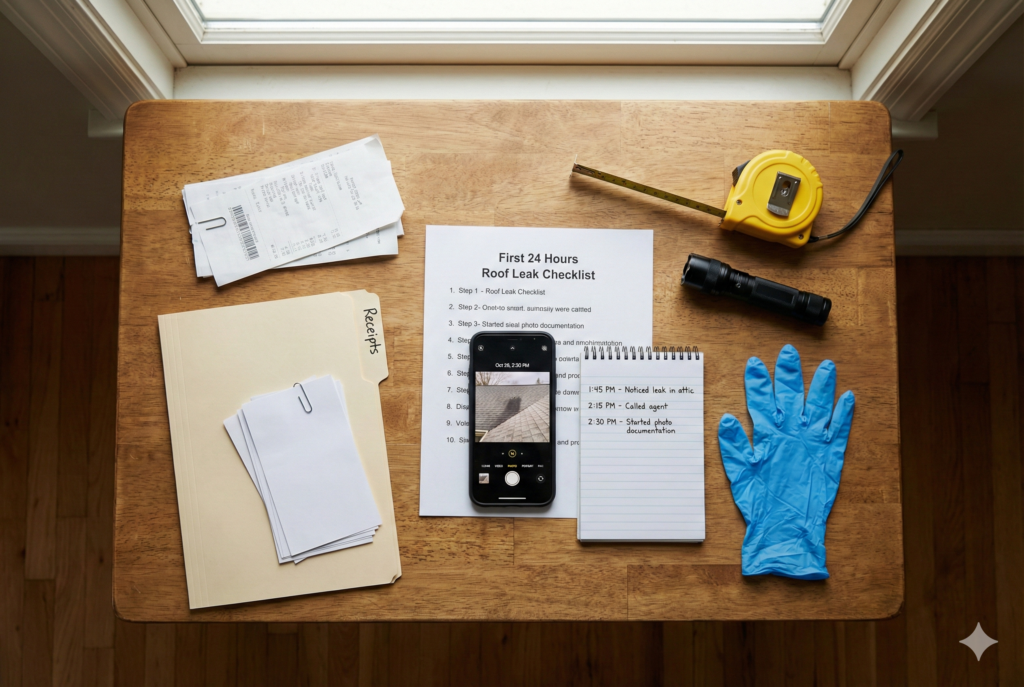

Below is a simple checklist for homeowners dealing with storm-related roof leaks, plus the exact photos and proof insurers typically want to see.

Need help right now? If you are dealing with a roof leak insurance claim in Atlanta and want someone on your side, call for a free consultation: Public Adjuster in Atlanta, GA

Before anything else – handle safety and stop the spread

Do these first. They protect your home and prevent the claim from getting messier.

- If water is near lights, outlets, or a ceiling fixture, avoid that area and consider shutting off power to the affected rooms.

- If a ceiling is bulging, do not stand under it. Water can pool and collapse drywall.

- Move what you can: electronics, rugs, furniture, and anything sentimental.

- Contain the leak: buckets, towels, plastic sheeting, and a drip path into a container.

- If water is spreading fast, call a water mitigation company. You are generally expected to take reasonable steps to prevent further damage.

The goal is not to “fix everything” in day one. The goal is to stabilize the situation and document the story clearly.

FEMA gives the same general guidance after property damage: document first, then clean or make temporary repairs, and save receipts.

The first 24 hours checklist (Atlanta roof leak edition)

Follow this order. It keeps your timeline clean and avoids common mistakes.

1) Start a claim log (5 minutes)

Open a note on your phone and write:

- Date and time you noticed the leak

- What rooms were affected

- What the weather was doing (wind, heavy rain, duration)

- What actions you took (buckets, shutoff, tarp, mitigation call)

- Who you spoke with and when

This sounds basic, but it is huge. The Georgia Office of the Commissioner of Insurance recommends keeping copies of correspondence and logging contact details and what was said.

2) Take photos and video before you touch anything (10 to 20 minutes)

Before cleanup, before fans, before moving soaked items if possible – document it. FEMA specifically recommends taking photos before cleanup and saving repair receipts.

Use the photo checklist later in this post so you do not miss key angles.

3) Do temporary mitigation (as needed)

Examples:

- Tarping a compromised roof area

- Placing plastic sheeting in attic (only if safe)

- Removing small amounts of standing water

- Starting drying equipment

Important: Temporary mitigation is usually fine and often expected. Just document before and after, and keep receipts.

4) Call the insurance company to report the claim (same day if possible)

When you report it:

- Ask for the claim number

- Ask what they need from you and when

- Ask when to expect an adjuster inspection

- Keep it factual (more on what to say below)

Georgia OCI guidance is straightforward: file as soon as possible and keep records of communications.

5) Get a roofing inspection (but be careful what you sign)

You can and should get a professional opinion. Storm damage can be obvious on the roof while the interior looks minor, or the reverse.

Just be careful with paperwork. If someone is pushing you to sign something you do not understand, slow down. If it feels like a “sign-now-or-else” situation, it is usually a bad sign.

6) Keep damaged materials when possible

Do not rush to throw away damaged items or materials until you have thoroughly documented them. FEMA even suggests keeping samples of certain materials when possible.

Exactly what to photograph and video (photos and proof insurers want)

Aim for “wide shots that tell the story” plus “close-ups that prove the details.”

Interior (every affected room)

- Wide doorway shot of the whole room (establishes context)

- Ceiling stain close-ups (capture edges and size)

- Walls: bubbling paint, staining, warped trim

- Flooring: cupping, buckling, wet carpet, soaked padding

- Baseboards and corners (water collects here)

- Personal property damaged (furniture, rugs, electronics)

Pro tip: put a common item in frame for scale (a tape measure, a coin, your hand) – just be consistent.

Attic (only if safe)

If you can safely access:

- Wet insulation

- Water trails on rafters or trusses

- Wet roof decking

- Daylight showing through (if present)

- Drip points and their path

If you smell electrical burning or see wet wiring, do not go in.

Exterior (from the ground is fine)

You do not need to climb your roof to be helpful. Photograph:

- Missing or lifted shingles

- Bent flashing

- Damaged vents or pipe boots

- Gutters pulling away

- Downspouts detached

- Debris impact points (tree limbs, blown objects)

“Proof” extras most homeowners forget

- Screenshots of weather during the time window (wind/rain)

- A short walkthrough video showing the path: exterior -> attic -> interior room

Covered vs not covered – the quick version (so you know what insurers are looking for)

This varies by policy, but most insurers generally draw the line like this:

- More likely covered: sudden, accidental damage caused by a covered peril (wind, hail, falling objects) that leads to a leak.

- More likely denied or limited: leaks tied to wear and tear, rot, long-term deterioration, or pre-existing maintenance issues.

Major carriers explain this pretty plainly. For example, Progressive notes roof leaks may be covered when caused by events like heavy wind or hail, but generally not when caused by wear and tear or rot. Allstate describes a similar idea: covered peril damage that leads to a leak may be covered, but wear and tear and lack of maintenance typically are not.

This is why your documentation matters so much. You are building the clearest possible “this happened, then this happened” timeline.

Deductibles – quick, honest reality check

Yes, your deductible usually applies. That means even when a claim is approved, you typically pay the deductible portion out of pocket before insurance covers the rest (subject to your policy terms).

Where homeowners get caught off guard is not the deductible itself. It is when:

- The scope is incomplete (hidden damage not included)

- The carrier frames it as wear and tear

- The interior damage is acknowledged but the roof repair is limited

A good documentation package helps reduce those “gray area” arguments.

Common mistakes that get roof leak claims underpaid (or denied)

These are the big ones:

- Not documenting before cleanup

Once it is cleaned, insurers can treat it like it was not that bad. FEMA’s guidance is to photograph before cleanup/repairs and keep receipts.

- Only photographing the stain, not the scope

You want wide shots plus close-ups, and you want to show every affected room, not just the “worst spot.”

- Throwing away damaged items too early

If it is not documented, it is easy to undervalue.

- Letting “wear and tear” become the story by accident

Homeowners sometimes say things like “Yeah the roof is old anyway.” Even if that is true, it can derail the claim narrative.

- Not keeping receipts and invoices

Georgia OCI specifically recommends not letting receipts pile up and keeping records.

What to say (and not say) when you call insurance

You do not need to play lawyer. Just stay factual.

Say:

- “We had heavy wind and rain, and I noticed leaking in [room] at [time].”

- “I have photos and video from before cleanup.”

- “I took temporary steps to prevent further damage and saved receipts.”

- “I would like an inspection scheduled as soon as possible.”

Avoid:

- Guessing the cause: “It must be the flashing” or “it has been leaking for months”

- Overstating: “The whole roof is destroyed” (unless it truly is)

- Filling silence with theories

Also, confirm things in writing when possible. Georgia OCI emphasizes keeping copies of correspondence and tracking who you spoke with and what was said.

When to bring in a public adjuster (especially in Atlanta)

A public adjuster represents you, not the insurance company. If any of the below are true, it is usually worth getting help early:

- Multiple rooms are affected, or there is attic damage plus interior damage

- The carrier is leaning hard on “wear and tear” language

- The first estimate feels too low, or key items are missing

- You are overwhelmed and do not want to manage the documentation battle

If you want a second set of eyes before you get boxed in by the process, start here: Public Adjuster in Atlanta, GA

Related: winter storm damage can show up late

If your leak showed up after a freeze-thaw cycle (common when materials expand and contract), this post is worth skimming too:

Winter Storm Fern Damage: What Happens to Your Home After the Snow and Ice Melt

FAQ: Roof leak insurance claim Atlanta

Q: What should I document first for a roof leak insurance claim in Atlanta?

A: Start with photos and video before cleanup, then write down the time you noticed the leak, what rooms are affected, and what temporary steps you took to prevent further damage.

Q: Can I tarp my roof before the insurance adjuster comes out?

A: Yes. Temporary mitigation is often expected to prevent further damage. Photograph the damage first, photograph the tarp after, and keep all receipts.

Q: Does homeowners insurance cover roof leaks from wind and rain?

A: It often can when wind or another covered peril creates damage that lets water in. Coverage is commonly disputed when the insurer claims wear and tear, rot, or long-term deterioration caused the leak.

Q: Should I wait to report the claim until I know how bad it is?

A: Usually no. Report promptly, keep records, and document thoroughly. Delays can complicate the timeline and communication trail.

Q: What if the insurance company underpays or I disagree with the settlement?

A: Ask for the specific policy language they are relying on, keep everything in writing, and consider escalating through consumer resources or professional claim help.