A house fire is one of the most overwhelming events a homeowner can experience. Between the emotional shock, displacement, and pressure to “get back to normal,” many people unknowingly make decisions that seriously reduce their insurance payout.

This matters more than most homeowners realize. In the U.S. alone, residential fires cause over $11 billion in direct property damage each year. And fire and lightning claims are among the most expensive insurance claims, averaging over $77,000 per claim.

Insurance companies move fast after a fire. If you are not careful, small missteps in the first days and weeks can permanently limit what you recover.

Here are seven of the most common and costly mistakes homeowners make after a fire and how to avoid them.

Mistake #1: Cleaning Up or Throwing Items Away Too Soon

After a fire, the instinct to clean up is natural. Unfortunately, this is one of the fastest ways to damage your claim.

Every damaged item is evidence. Once it is thrown away, it is gone for good. Insurance companies rely on documentation to justify payment. If an item is not documented, it often does not exist in the claim.

This is especially dangerous with:

Smoke-damaged contents

Electronics that appear intact

Structural materials behind walls or ceilings

Smoke damage alone can represent a significant portion of a fire claim. Many homeowners do not realize that smoke can cause long-term corrosion, odor absorption, and health risks, even in areas untouched by flames.

What to do instead:

Do not discard anything without documenting it thoroughly. Photograph and video all damage before any cleanup begins. When possible, store damaged items until they have been properly inventoried.

Mistake #2: Not Creating a Detailed Personal Property Inventory

Insurance companies do not pay based on what you remember owning. They pay based on what you can prove.

Many homeowners submit vague inventories like “clothes,” “furniture,” or “electronics.” That language works against you. A couch is not just a couch. It has a brand, age, material, size, and condition. The same applies to nearly every item in your home.

When inventories are vague, insurers often default to the lowest reasonable valuation.

This matters because fire claims frequently involve tens of thousands of dollars in personal property losses, especially when smoke damage is widespread.

What to do instead:

Create a room-by-room inventory with:

Item descriptions

Approximate age

Original quality or brand

Replacement value when possible

The more specific the inventory, the harder it is for an insurer to undervalue it.

Mistake #3: Assuming the Insurance Company’s Estimate Is Complete

The first estimate is rarely the final or full scope of damage.

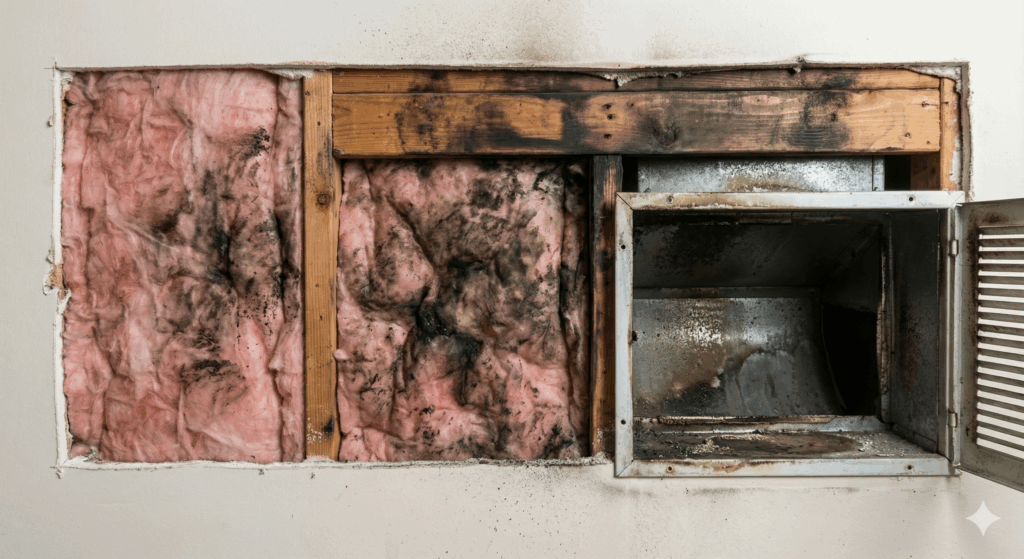

Insurance adjusters often inspect quickly and focus on visible damage. But fire losses are rarely simple. Hidden damage behind walls, in insulation, ductwork, wiring, and framing is extremely common.

This is especially true when smoke spreads beyond the fire origin. According to national fire data, smoke damage affects far more of a home than flames alone in most residential fires.

If damage is not included in the initial scope, it may never be paid.

What to do instead:

Treat the first estimate as a starting point, not a conclusion. A proper fire claim should consider:

Structural damage

Smoke migration

Odor penetration

Code upgrades

Temporary repairs and protective measures

Mistake #4: Ignoring Rebuild Cost Inflation

Construction costs have increased significantly in recent years, and many policies have not kept up.

Reconstruction costs rose over 4 percent in a single year according to Verisk, driven by material prices and labor shortages. Some regions have seen even higher increases depending on demand and contractor availability.

If your policy limits were set years ago, they may not reflect today’s real rebuild costs. Settling early without addressing this gap can leave homeowners paying out of pocket later.

This problem is widespread. A study of homeowners affected by the Marshall Fire found 74 percent were underinsured, with over one-third severely underinsured relative to rebuild costs.

What to do instead:

Review coverage limits carefully and do not assume they are sufficient. Make sure estimates reflect current labor and material pricing, not outdated assumptions.

Mistake #5: Overlooking Smoke and Soot Damage in “Unaffected” Areas

Smoke does not respect room boundaries.

Even rooms that look untouched may suffer from:

Soot infiltration

Embedded odors

HVAC contamination

Long-term corrosion of electronics and appliances

Insurance companies sometimes downplay smoke damage because it is harder to see and measure. But untreated smoke damage can lead to ongoing health issues and permanent odor problems.

Residential fire data consistently shows that smoke damage often represents a large portion of total loss, especially in cooking-related fires, which are the leading cause of home fires nationwide.

What to do instead:

Ensure smoke-affected areas are properly evaluated and included in the claim. This includes testing, cleaning, sealing, and in some cases full replacement of affected materials.

Mistake #6: Missing Deadlines or Failing to Communicate in Writing

Fire claims involve deadlines, documentation requests, and ongoing communication. Missing a deadline or relying on verbal conversations can weaken your position.

Insurance claims are paper trails. When something is not documented, it is easier for it to be delayed, denied, or forgotten.

What to do instead:

Keep copies of all correspondence

Confirm conversations in writing

Track submission dates and deadlines

This creates accountability and protects you if disputes arise later.

Mistake #7: Settling Before the Full Scope of Damage Is Known

One of the most damaging mistakes is settling a claim too early.

Once a claim is settled, reopening it can be extremely difficult, even if new damage is discovered. This is especially risky with fire losses, where hidden damage often emerges weeks or months later.

Insurance companies may push for early resolution. For homeowners under stress, that can sound appealing. But speed often comes at the expense of completeness.

What to do instead:

Make sure the full scope of damage is identified and documented before agreeing to settlement terms. This includes repairs, contents, temporary living expenses, and long-term remediation needs.

Getting the Claim Right Matters

A fire insurance claim is not just paperwork. It determines whether you can fully recover or are forced to absorb losses you thought were covered.

Given the complexity and high dollar value of fire claims, even small mistakes can translate into tens of thousands of dollars left unpaid.

If you are navigating a fire damage claim and want to be sure nothing is missed, having an experienced advocate review the claim can make a meaningful difference. A second set of trained eyes can help ensure the scope, documentation, and valuation reflect the true impact of the loss, not just what is easiest to measure.